Underwriting headcount is a slow lever. Origination volume is not. When a lender’s pipeline fills up faster than its underwriting team can move, the usual fix is hiring. But hiring takes months, and if the market turns before those new hires are trained, the lender is left paying for capacity it no longer needs.

An East Coast based independent mortgage bank with a servicing portfolio exceeding $600 billion ran into exactly this. The lender operates across consumer-direct, wholesale, and correspondent channels and, as a leading aggregator, offers Conventional, FHA, VA, USDA, and other mortgage products. New originations were piling up. Turn times were slipping because there simply weren’t enough underwriters to keep pace.

Adding staff carried its own risk. More underwriters under more pressure is a formula for mistakes, and the lender knew it. Market conditions weren’t helping either. Hiring into an uncertain rate environment meant a real chance of having to lay people off a year later. The lender needed more throughput without a bigger headcount and without a bigger cost base.

Where DecisionGenius came in

The lender turned to

DecisionGenius for automated underwriting rather than staffing up to meet demand. This kind of mortgage underwriting automation started with Conventional loans, expanded to FHA loans, and has now moved into an optimization phase.

For a CEO or COO, the real shift here isn’t technical. It’s what happens to the hiring conversation. A forecast-driven hiring decision carries risk in both directions, too many people or too few. Automating the underwriting work already inside the building sidesteps that bet entirely. The lender didn’t need to guess right about volume. It needed more capacity from the team it already had, and that’s what it got.

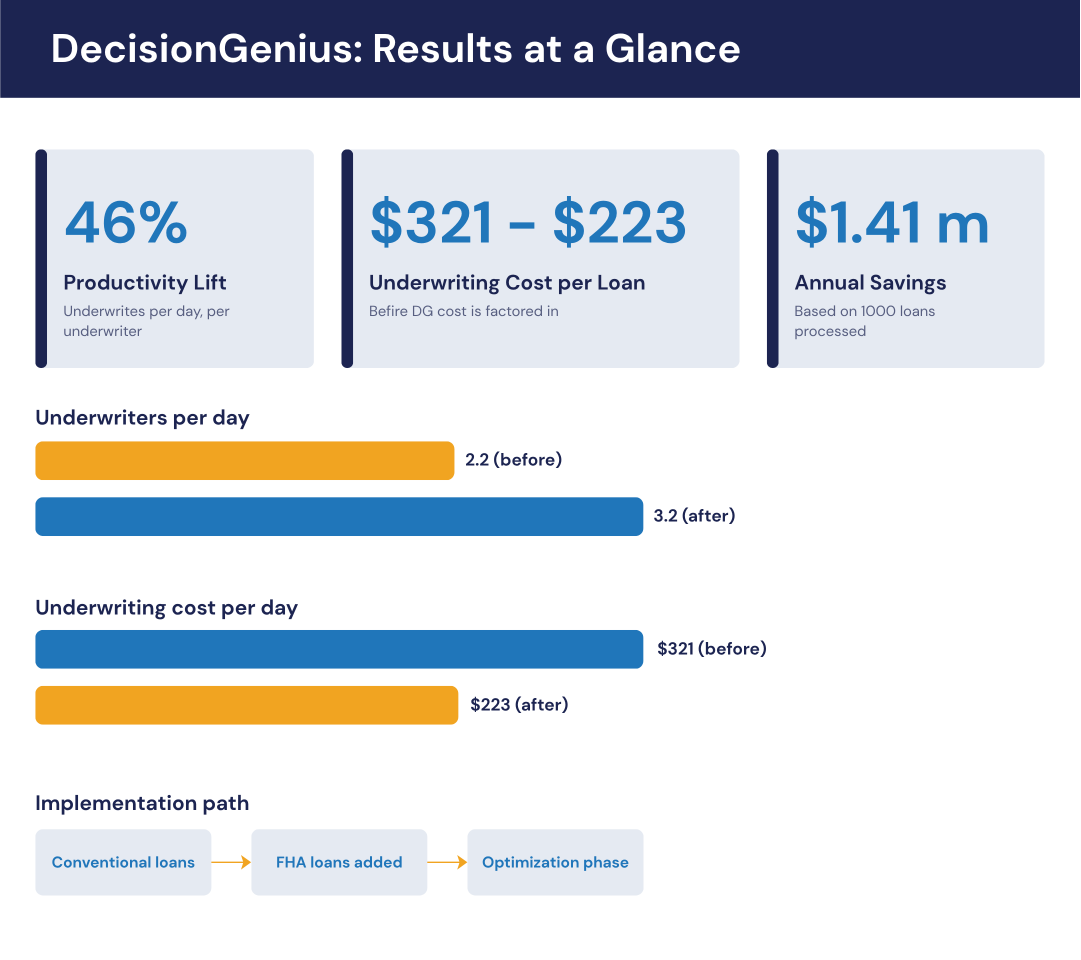

The order of the rollout says something too. Conventional loans came first, the most standardized product the lender writes, which gave the team a controlled way to see the platform in action before expanding it. FHA loans followed. Optimization is where the lender sits now, tightening what’s already running rather than pushing into new products.

What the numbers show

Underwriter productivity moved first. Before

DecisionGenius, underwriters closed 2.2 loans a day. After implementation, that number reached 3.2, a 46 percent lift. The lender is targeting 4.2 loans per day as optimization continues, so this gain came before the platform was even fully tuned.

Cost followed the same trajectory. Underwriting cost per loan fell from $321 to $223, a figure that doesn’t yet include the cost of DecisionGenius itself. Across 1,000 loans, factoring in the corporate overhead the underwriting department carries based on its FTE count, that gap works out to roughly $1.41 million a year.

Two things happened at once here, and that’s what makes the result worth paying attention to. Output went up. Cost went down. Neither came at the expense of the other, and neither required a single new hire. That combination is what most lenders are really trying to find when they look at an AI mortgage underwriting system.

The rollout order was the point

The lender didn’t flip a switch across its whole loan book. Conventional loan came first, FHA came after results held up, and optimization is where things stand now, not a further expansion. That order gave the lender room to trust the results before leaning on them harder.

It’s also worth noting these numbers aren’t the ceiling. The lender’s own target is 4.2 underwrites completed per day per underwriter, and the platform hasn’t gotten there yet. The 46 percent lift and the $1.41 million in savings happened on the way to that number, not after reaching it.

What it means for other lenders

Pipeline volume doesn’t wait for a hiring plan to catch up, and in a market this jumpy, adding headcount is a bet few lenders want to make right now. This lender’s approach to automated mortgage underwriting didn’t touch headcount at all. It automated the underwriting work sitting inside the team it already had, rolled out one loan type at a time, with results checked at every step.

The productivity lift and the cost savings matter on their own. What matters more is that they happened together, before the platform was fully optimized, without adding a single underwriter. That’s the outcome worth measuring against.