Solutions

I AM A

I NEED

Company

Solutions

I AM A

I NEED

Company

|

$11558

|

47 Days

|

~40%

|

44-46 days

|

|---|---|---|---|

|

Average cost to originate one loan Source: MBA IMB Performance Report, Q1 2025 |

Average time to close, industry wide Source: MBA / ICE |

of underwriter time on non-decisioning tasks Source: STRATMOR Group, 2025 |

average time to close a purchase loan Source: ICE Mortgage Monitor, 2025 |

|

Task

|

Est. Time Share

|

AI Workbench Impact

|

|---|---|---|

|

Stare-and-compare / data re-entry

|

15-20%

|

Up to 80% reduction

|

|

Condition management and tracking

|

10-15%

|

Automated queuing and status tracking

|

|

Document review and classification

|

10-12%

|

60-70% faster with intelligent document processing

|

|

TRID / ATR / HMDA compliance checks

|

8-10%

|

Embedded, real-time, no separate step

|

|

Borrower and file research

|

5-8%

|

One-click summaries with source citations

|

|

Actual credit and risk decisioning

|

30-35%

|

Amplified, not reduced

|

|

Capability

|

Standalone AI Tool

|

Indecomm Genius AI Suite Workbench

|

|---|---|---|

|

Loan file intake

|

Manual pre-processing required

|

Multi-format ingestion, auto-indexed

|

|

DU / LP overlay management

|

Separate manual review

|

Flagged findings surfaced in-flow

|

|

Condition management

|

Email and spreadsheet tracking

|

Automated queuing with aging visibility

|

|

TRID / compliance checks

|

Done late, manually

|

Embedded at the correct workflow stage

|

|

Underwriter guidance

|

None

|

Next-best-action prompts and risk flags

|

|

Audit trail

|

Assembled after the fact

|

Logged and traceable by default

|

|

Team collaboration

|

Email hand-offs

|

Integrated task routing and escalation

|

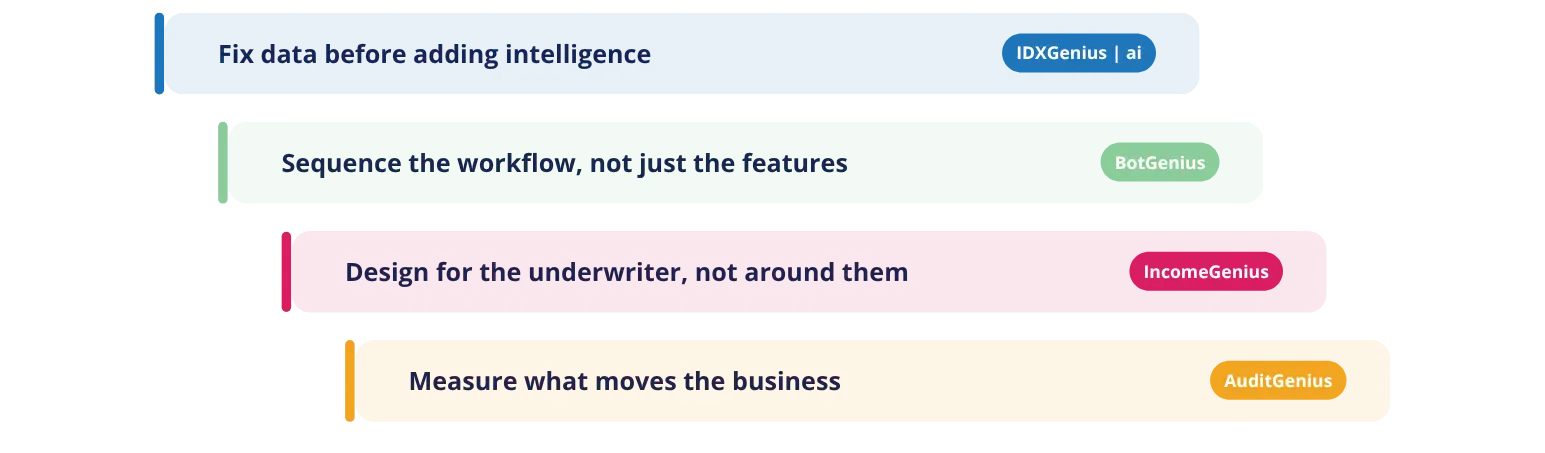

In practice, that means a few non‑negotiables:

That is the design center for Indecomm’s Genius AI suite, anchored by DecisionGenius, the AUS workbench that puts credit, income, assets, and collateral in one place so underwriters have everything they need to make the call without switching systems. DecisionGenius pulls in income analysis through IncomeGenius and document data through IDXGenius|ai, so by the time a file reaches the underwriter, the numbers are already calculated, the docs are already classified, and the AUS findings are already surfaced in context. AuditGenius closes the loop on quality and compliance, and BotGenius keeps files moving between stages without manual hand-offs.

[ninja_form id=2]