Mortgage lending in 2026 is an industry caught between what AI-powered mortgage underwriting can do and what most lenders have actually gotten it to do. A recent

National Mortgage News survey found that 57 percent of mortgage professionals believe AI-powered mortgage underwriting will create the greatest industry change this year. Adoption of AI and machine learning among mortgage lenders has more than doubled in two years. The technology investment is real. The contracts are signed. The systems are live.

And yet in operation after operation, the loan quality outcomes and productivity gains that so many mortgage underwriting platforms promised have not materialized to the extent that was expected. Files still arrive at the underwriter’s desk incomplete. Conditions are still being cleared manually. The documents are still not automatically pulling into the AUS, which leaves data when it comes time for an underwriting decision. The gap between AI-powered underwriting’s capability and its actual deployment in mortgage banking is one of the defining operational challenges of 2026.

This is not a technology failure. It is the most common mortgage AUS implementation story amongst mortgage lenders. The automated underwriting system works. The AUS adoption plan did not.

The Business Case Has Shifted and Both Versions Point the Same Direction

It wasn’t all that long ago that the dominant question in mortgage operations was capacity: how do we close more loans? There have been times when volume set the agenda. When pipelines were full and underwriter headcount could not keep pace, automation was one possible answer to a throughput problem that hiring alone could not solve. And, for many, it did in fact solve some of those challenges.

But, the market shifted. That question has since been replaced by a harder one with AI-powered underwriting is at the center of it: How do we manufacture each mortgage loan more precisely, every time, at a cost structure that holds regardless of where rates go? The shift is not just operational. It is structural. The average cost to produce a mortgage in 2025 was approximately $11,800 per loan according to the Mortgage Bankers Association. Loan quality problems, rework, and late-stage conditions are not just process friction, they are measurable margin loss on every file. The AI tools now available to mortgage lenders can address this directly: reading unstructured documents, synthesizing data across multiple sources, flagging exceptions before they become conditions, and surfacing loan decisioning logic that used to live exclusively in an underwriter’s head. The question is no longer whether to deploy these capabilities. It is how to deploy them in a way that actually changes loan quality and cost outcomes.

Cost per loan, number of touches, and cycle time are boardroom metrics now, not just operations numbers. The tolerance for processing inefficiency that volume once covered is gone. It does not come back regardless of where rates go and the mortgage lenders who understand that are building operational infrastructure designed to perform in any market, not just a busy one.

Here is what the most forward-thinking lenders have already worked out: mortgage quality and borrower experience are not competing objectives. As Indecomm CEO Rajan Nair puts it:

Operational precision and borrower experience move together. Faster turnaround times, fewer conditions, and less back-and-forth on the mortgage loan file means better pull-through. The same investment that lowers cost-per-loan shortens the borrower’s timeline. Generative AI, deployed with the right mortgage underwriting platform, a smart document and data extraction strategy, and the right adoption plan, is what makes both possible at scale.

AUS Technology Has Come a Long Way, and Generative AI Is the Next Chapter

The starting point for automated underwriting was the GSE systems: Fannie Mae’s Desktop Underwriter and Freddie Mac’s Loan Product Advisor. For a long time, that was the ceiling on what AI-powered underwriting could do in mortgage banking.

The real shift came in the last eight to ten years, as mortgage lenders began targeting specific components of the loan underwriting decision. Income was the first major opportunity. As document quality and data integrity improved, automation potential grew with it. Machine learning, OCR, and XML-based data processing became the foundation of what a modern AUS platform can do for mortgage quality and operational efficiency. As a growing AUS provider to the mortgage industry, Indecomm built its

DecisionGenius solution to address these challenges, embedding its

IncomeGenius solution and components of its

IDXGenius | ai technology into the loan decisioning platform.

Now generative AI is opening the next chapter. As Nair explains:

The mortgage industry’s AI capabilities now exceed how most lenders are actually applying them. The gap is not technical, it is organizational. And the mortgage lenders positioning themselves well are asking a harder question than what AI-powered underwriting can automate. They are asking what it takes to deploy AI responsibly in loan decisioning. Nair is direct on this:

That distinction matters especially as GSE AI governance mandates have moved from guidance to requirement. Freddie Mac and Fannie Mae now require mortgage lenders to disclose the AI tools in use, their providers, and the safeguards in place to mitigate risk. The obligation falls on the lender, not the vendor. A generative AI layer in a mortgage underwriting platform that cannot produce auditable reason codes, explainable outputs, or traceable loan decisioning logic is not a productivity tool. It is a compliance liability.

For lenders evaluating AUS platforms with generative AI components, the core question is not what the system can automate. It is how the system documents what it decided and why. Guardrails are not optional part of the equation. They are built on business rules and in-depth mortgage banking process knowledge; i.e., guardrails are the equation.

What “Automated Underwriting” Actually Covers

Artificial intelligence

AI covers a spectrum, from a simple internal chatbot to a system that influences an actual mortgage loan decisioning outcome. The threshold question is how comfortable the organization is with AI making or influencing credit decisions, and where human review must remain essential. That answer shapes every other evaluation question that follows.

Data and document confluence

This is the functional core of any serious mortgage underwriting platform. The capability here has to outperform what a skilled human does manually: extracting, organizing, and comparing documents with data for accuracy, using technologies like OCR, machine learning, XML, and business rules engines. It is worth asking whether this capability or at least aspects of document intelligence is built natively by the vendor or licensed from a third party, because experience in mortgage document processing compounds over time.

This is also where the downstream argument for mortgage quality begins. Nair frames it as a pipeline problem:

The practical consequence for loan quality is significant. When a mortgage lender starts with clean, validated document data at origination, that accuracy travels downstream through loan underwriting, QC, and closing. Data problems caught late in the mortgage process are expensive. Data problems that never enter the process are free. A strong document processing solution at the front end of mortgage origination is not a preprocessing nicety. It is the foundation that determines the accuracy of every AI-powered underwriting decision that follows. Indecomm clients have found that using both IDXGenius | ai and DecisionGenius side-by-side offers an optimal combination.

Software and workflow integration

This covers the connectors: bidirectional APIs, LOS integration, conditions clearing, and reps and warrants. A pre-built LOS integration is a meaningful advantage for any mortgage underwriting platform implementation, particularly for technology teams without bandwidth for new builds. As Nair notes:

Intelligent automation

This is the loan decisioning engine — the layer that overlays business rules, machine learning, and document intelligence to generate, flag, and clear mortgage conditions. This is where the real loan quality and efficiency gains are realized, but only when the data feeding the engine is clean.

No mortgage underwriting platform covers every component equally, and no AUS addresses all four C’s of loan underwriting completely: credit, capacity, capital, and collateral. Harris is direct about where to start:

Build the must-have list and evaluate mortgage underwriting platforms against it.

Black Box or Glass Box: This Choice Shapes Everything

Two architectural approaches define the AUS market.

Black box mortgage underwriting systems — DU and LPA among them — process inputs and return outputs without showing the underlying loan decisioning logic. The advantages are real: simplicity, ease of use, limited need for underwriter intervention. The tradeoffs are also real: limited customization, low visibility into how mortgage quality decisions are made, and what practitioners call underwriter uncertainty. When mortgage underwriters cannot see why a condition was generated, trust in the AI-powered underwriting system erodes. And trust is what drives adoption.

Glass box mortgage underwriting platforms like DecisionGenius show how every loan decisioning step was made. Auditable, verifiable, customizable to unique loan underwriting requirements and reps-and-warrants commitments. The mortgage quality and productivity potential is higher, but the adoption challenge is more pronounced. As Harris cautions:

Managing that tendency is a change management problem rather than a problem with the tech.

The regulatory case for visibility in AI-powered underwriting has become unavoidable. In early 2026, both Freddie Mac and Fannie Mae moved AI governance for mortgage lenders from guidance to requirements. Freddie Mac’s rules took effect March 3, 2026. Fannie Mae followed with Lender Letter LL-2026-04, issued April 8, with requirements taking effect August 6. As HousingWire reported:

The liability falls on the mortgage lender regardless of which vendor’s AI is doing the loan underwriting work. Fannie Mae’s guidelines make this explicit: lenders and servicers will be held responsible for mistakes and noncompliant AI use by subcontractors and vendors, and are required to mandate appropriate supervision of those providers. Mortgage lenders will be expected to quickly disclose the types of AI-powered underwriting tools in use, their providers, and the safeguards in place upon inquiry from the GSE. [2][5]

The CFPB has been equally direct. Under ECOA and Regulation B, a creditor cannot use black-box loan underwriting technology when doing so prevents them from providing specific and accurate reasons for adverse action. If the AUS cannot explain its loan decisioning, the mortgage lender cannot legally stand behind it. [6]

For lenders evaluating mortgage underwriting platforms, this creates a practical three-part test: Can the system produce an auditable trail of how every condition was generated? Can it satisfy an examiner’s request for adverse action documentation? Can it support a lender’s own compliance monitoring obligations under the new GSE frameworks?

A glass box AUS architecture addresses all three directly. When every loan decisioning step is traceable to a specific data point or document comparison, the mortgage lender has the documentation the GSEs require, the reason codes ECOA demands, and the internal visibility needed to monitor AI-powered underwriting system performance over time. This is not a future consideration. It is a current requirement, and selecting a mortgage underwriting platform that cannot meet it today is a structural risk.

Neither approach is universally right. But the regulatory environment has shifted the calculus significantly. The right choice depends on loan underwriting culture, compliance requirements, and the adoption strategy a mortgage lender is prepared to execute — and those compliance requirements have grown considerably more specific in the past twelve months.

Run the AUS Earlier Than You Think

Most mortgage lenders default to running the AUS at submission to loan underwriting. That is one option but often not the best one.

Running the automated underwriting system at first document receipt makes mortgage processing the primary beneficiary. As Harris explains:

Files arrive at loan underwriting more complete, and conditions that would have been caught at the underwriter’s desk get cleared earlier in the mortgage process. The trend is toward moving even earlier amd toward the point of sale. Loan officers gain eligibility signals before a full application is submitted, which changes the borrower conversation and reduces the number of incomplete mortgage files that enter the pipeline in the first place.

This also reinforces the mortgage quality argument. The earlier accurate document data enters the loan underwriting workflow, the more it shapes every AI-powered underwriting decision that follows. Errors introduced upstream compound. Precision introduced upstream compounds equally. Running the AUS early only delivers its full value when the document processing feeding it is equally reliable.

The mortgage channel shapes the approach as well. A branch model, where originators have more autonomy, favors earlier and more distributed AUS deployment. A centralized consumer-direct model consolidates that function. The right mortgage underwriting platform should be capable of running at any stage of the loan lifecycle and carrying findings forward as the file moves through each phase.

On Fraud: A Real Advantage, With a Growing Threat

AI-powered underwriting systems run consistency cross-checks across the mortgage loan file at a scale no human team can match. They verify whether figures are consistent across documents, flag data conflicts that warrant escalation, and surface loan quality risks that manual review misses.

The threat, however, has changed in kind, not just in scale. Generative AI has made it materially easier to produce fraudulent documents that are visually indistinguishable from legitimate ones. Altered pay stubs, synthetic bank statements, fabricated employment verifications are no longer the work of sophisticated organized fraud rings. They are accessible to individual bad actors with modest technical capability. Mortgage fraud risk rose more than eight percent year over year in 2025. The document that arrives in a mortgage loan file today may have been generated, not scanned.

This is the offensive use of the same technology the mortgage industry is deploying defensively. And it raises the stakes for what document intelligence and QC platforms must be able to do to protect mortgage quality.

As Harris notes about traditional automated review:

That framing held when the threat was human manipulation of physical documents. The emergence of AI-generated fraud in mortgage lending requires a different posture: using AI on the offensive in QC, not just the defensive.

The answer is not more manual review. Human reviewers are not equipped to detect synthetic documents consistently, and mortgage loan volume makes comprehensive manual review operationally impossible. The answer may actually be that AI-powered QC solutions be built to interrogate mortgage documents at a depth no human reviewer can replicate: cross-referencing metadata, detecting statistical anomalies in formatting and typography, comparing document characteristics against known baselines, and flagging mortgage loan files that warrant escalated human scrutiny.

This is where a purpose-built document intelligence approach like

IDXGenius | ai and one trained on years of mortgage-specific document data rather than a general-purpose model carries a structural advantage. The ability to recognize what a legitimate W-2 looks like across thousands of employers and formats is not something a general model develops quickly. It is built through deliberate, longitudinal training on the real mortgage document universe that lenders actually process. That depth of training is what separates a genuine mortgage quality control capability from a general-purpose AI layer bolted onto a loan underwriting workflow.

How to Select the Right Mortgage Underwriting Platform: Start With Objectives, Not Features

Mortgage lenders who end up with the wrong AUS almost always made the same mistake: they evaluated features before they defined goals. Nair is candid about the noise in the market:

Cutting through it starts with setting clear, measurable loan underwriting objectives before any vendor conversation begins. A concrete example: an underwriting team processing 2.5 loans per day needs to reach 4 or 5. That single goal drives the right questions about any mortgage underwriting platform. Can this AUS deliver a clean mortgage file early in the process? Can it run with minimal documentation at origination? Can it automate the specific loan conditions that matter most to this operation?

Building a cross-functional committee is equally important. Operations alone should not make this call. Technology and credit risk need to be at the table to ensure the right decision and the organizational buy-in that follows. Mortgage underwriting platform implementations with cross-functional commitment from the start consistently outperform those that do not.

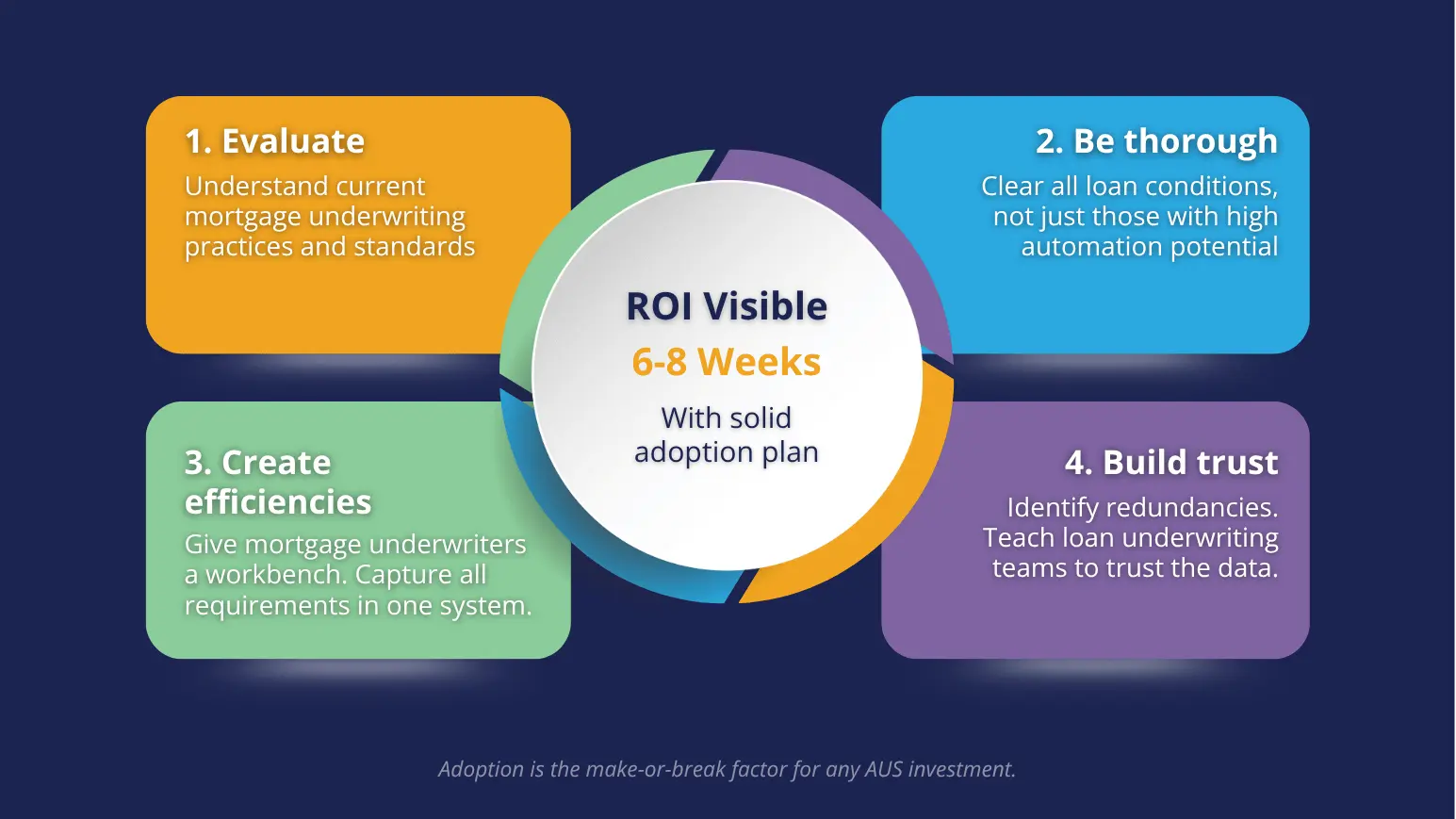

Adoption Is What Makes or Breaks the AUS Investment

ROI from an automated underwriting system typically appears within 6 to 8 weeks. But only when there is a structured adoption plan in place. Without one, even the right mortgage underwriting platform stalls. Industry research consistently points to the same pattern: AI initiatives in mortgage banking fail not because of technology gaps but because of cultural and operational barriers. The technology goes live. The humans do not change. And six months later, no one can explain why the loan quality and efficiency gains have not arrived.

As Nair puts it:

A 2026 survey of mortgage and real estate professionals found that more than half use AI for support only and exclude it from final loan decisioning, not because the technology is incapable, but because the trust has not been built. That trust gap is the real AUS implementation challenge, and it is a leadership and change management problem, not a software problem.

Mortgage underwriters are not naturally inclined toward new AI-powered underwriting tools, and the reason is rarely about competence. It is about professional identity. An underwriter who has built a career on judgment can feel exposed when an AUS generates the loan underwriting conditions they used to derive themselves. That concern has to be addressed directly and early.

The reframe that consistently works is positioning the AUS as a workbench, not a replacement. In Nair’s words:

The mortgage underwriter arrives at a prepared file and applies expert judgment to what remains. That is not a diminished role. It is a more productive one. Reps and warranties matter here more than most lenders expect. Harris is precise about why:

That certainty functions as an adoption accelerator. It gives mortgage underwriting teams the confidence to trust the AI-powered underwriting output and move forward.

The four-step adoption cycle that drives AUS ROI:

The Bottom Line

The mortgage industry entered 2026 with more AI-powered underwriting capability than it has ever had, and more implementations falling short of their potential than anyone expected. That gap is not necessarily a technology story. It never was. The automated underwriting system works. What fails is the groundwork that has to happen around it: the clear objectives set before a vendor is selected, the cross-functional buy-in built before go-live, the adoption plan executed with the same rigor as the implementation itself.

The capability is there. The ROI is documented. The path is clear. What separates the mortgage lenders who realize it from those still waiting on results is not the platform. It is the work.

Clean data at origination. A mortgage underwriting platform selected against specific loan quality objectives. An adoption plan that addresses the human side with the same discipline as the technical side. These are not complicated ideas. They are unglamorous ones. And in 2026, they are the difference between an AUS investment that pays off and one that sits underutilized while the market moves on.

Loan quality does not improve because a mortgage underwriting platform is running. It improves because the people using it trust it, the processes feeding it are clean, and the leaders responsible for it treated adoption as the investment, not the afterthought.

The lenders who will look back on 2026 as the year they gained a durable operational advantage are not the ones who moved fastest. They are the ones who got it right.

Works Cited

- Consumer Financial Protection Bureau. Using Artificial Intelligence in Automated Underwriting Systems: Adverse Action Notice Requirements Under ECOA and Regulation B. Consumer Financial Protection Circular, 2024.

- Fannie Mae. “Governance Framework on Use of Artificial Intelligence and Machine Learning.” Lender Letter LL-2026-04, 8 Apr. 2026.

- Freddie Mac Guide. “AI Risk Management Requirements.” Single-Family Seller/Servicer Guide, Bulletin 2025-16, §§ 1302.2 and 1302.8, 3 Dec. 2025 (Effective 3 Mar. 2026).

- Freddie Mac Single-Family. Cost to Originate Study: 2025 Updates and Technology Metrics. Operational Performance Report, 2025.

- Indecomm Global Services. “From Document Automation to Document Intelligence.” Indecomm Thought Leadership Articles, 19 May 2026.

- Stratmor Group. Mortgage Technology Insight Study. Corporate Strategy and Technology Report, 2025.