Mortgage lenders have spent heavily on AI and automation over the past three years. The results have been uneven. What most vendors delivered were tools that needed months of setup, heavy IT involvement, and change management cycles that drained the very teams they were supposed to help. Deploying AI without fixing the underlying workflow is not transformation. It is pouring concrete over a crack. The investment stalls, adoption lags, and the ops team is left holding a system that was never built around how they actually work.

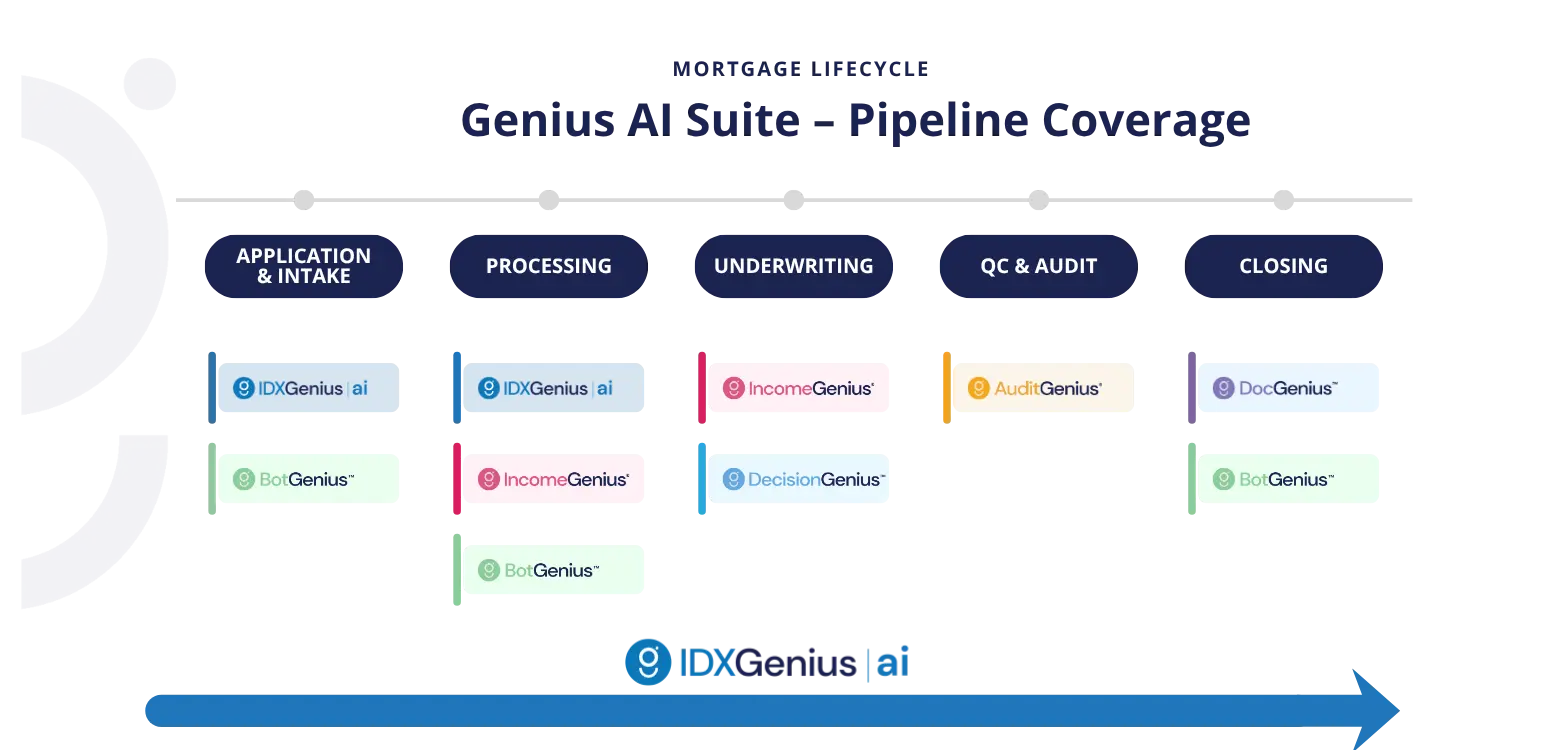

Indecomm built the Genius AI Suite from a different starting point: not how to apply AI to mortgage, but where mortgage work actually breaks down. Six products came out of that thinking, each targeting a specific workflow, together covering the full loan lifecycle from document intake to audit review.

A Fully Manual Process Creates Risk

$11,558

avg. cost

to originate one loan

(MBA, IMB Report Q1 2025)

68%

of lenders cite manual doc review

as top ops bottleneck

(ICE Mortgage)

40%

of loan defects tied

to income calc errors

(Fannie Mae)

2.5x

faster cycle times with

AI-assisted processing

(Indecomm client data)

The Problem with One-Size-Fits-All AI

Most enterprise AI platforms are built for flexibility. That sounds like a powerful feature. In practice, it means the mortgage team has to configure everything: the document types, the decision logic, the exception workflows. However, this means the vendor provides the engine while the lender provides the expertise to make it run; creating more work for the lender in the end. That model may work for banks with large technology teams but for most mortgage companies, it creates a different problem: skilled operations staff are pulled into implementation work instead of loan production. Six months into a deployment, adoption is low, processing times have not moved, and the business case is hard to defend.

Indecomm designed the Genius AI Suite as purpose-built tools. Each product arrives with the mortgage workflow already built in (designed by mortgage experts). There is no blank-slate configuration. You connect it to your LOS, set your parameters, and it works.

Six Products. One Loan Lifecycle. Here's How They Fit

The six products in the suite map to six distinct points of friction in the mortgage process. Here is how each one fits.

Why Mortgage-Specific Design Matters

A general-purpose AI document tool can read text. IDXGenius |ai knows that a 1003, a paystub, and a tax transcript each carry different data structures, different errors, and different downstream implications. That difference matters when your processor is reviewing 15 loans at once and cannot afford to chase misclassified documents.

The same logic applies to income. IncomeGenius was built around GSE income calculation guidelines, not generic financial analysis. When a borrower is self-employed with two years of Schedule C income and a partnership K-1, the tool knows how to handle that. A general AI model does not, at least not without significant customization.

There is a downstream effect that often goes unacknowledged in AI ROI discussions. When documents are processed, organized, and extracted accurately at intake, that precision carries through every stage that follows. Fewer defects at underwriting. Fewer surprises at closing. Less rework across the board. AI does not just move work. Done well, it cleans the pipeline.

Intelligent document solution is applicable at every stage of origination and beyond.

The Integration Question

Lenders ask two things before any AI deployment: does it connect to our LOS, and who manages it after go-live.

The Genius Suite integrates with the major loan origination systems including Encompass, Empower and, OpenClose. The architecture uses a bi-directional API connector, which means changes on the LOS side do not require a full reintegration. Additionally, the flow of documents and data are both to and from the LOS, so data is aligned between systems. Finally, the API connector allows the Genius Suite to connect to any LOS.

On the management side, Indecomm offers its Mortgage Operations services alongside the tech suite. That is relevant for shops that want to deploy AI without expanding their internal tech headcount. The managed services team handles model updates, exception review, and performance monitoring. The lender’s operations team focuses on loan production.

That combination, purpose-built AI with an experienced ops services layer, is what Indecomm calls its full-stack model. It is designed for lenders who want outcomes, not software to manage.

How Lenders Are Using the Suite

Most lenders do not deploy all six products at once. The more common pattern is to start with the workflow that is costing the most time or creating the most defects, prove the model, and expand.

What Practical AI Actually Looks Like

There is a version of AI adoption that looks impressive on a slide and does not move the numbers. Lots of mortgage companies have been through it. The Genius Suite was built to avoid that.

Practical AI in mortgage means the processor does not have to recheck every document the system touched. It means the underwriter opens a file and the income calculation is already done, with the source documents mapped. It means the QC team reviews exceptions instead of every loan in the pipeline. That is a narrower definition than what most AI vendors sell. It is also more useful. The goal is not to automate the mortgage process. The goal is to remove the parts that slow it down and cost the most when they go wrong.

What shifts as a result is where human effort goes. Document-heavy tasks like data entry, indexing, and validation move to the system. The processor moves up: toward exception handling, borrower experience, and loan quality review. That is not a reduction in the value of ops staff. It is a redefinition of their work toward what requires judgment rather than repetition.

That shift also comes with a responsibility. Retraining someone who has spent fifteen years validating documents by hand to oversee the system doing it requires more than a new software license. Organizations that ignore that human dimension will find their AI investments collecting digital dust regardless of how good the technology is.

The MBA’s IMB 2025 report put average origination costs at $11,558 per loan. Most of that cost lives in labor: processing, underwriting, QC, and closing. The Genius Suite targets each of those specifc areas directly. That is the design logic behind building six specific targeted products instead of a blanket AI solution.

The Business Case in Plain Terms

The ROI on any AI deployment in mortgage comes down to three numbers: how much it costs to run, how much it reduces per-loan cost, and how fast it pays back. Indecomm publishes client outcome ranges rather than guarantees, which is the right approach.

Based on documented client deployments, lenders using multiple products across the suite have seen per-loan cost reductions of 35-45% depending on the solution implemented, volumes, and adoption rates.

What does not vary is the logic. If your document processing team spends three hours per loan on intake work that IDXGenius | ai handles in minutes and with greater accuracy, the math is not complicated.

The institutions that will lead this shift are not the ones chasing the fastest deployment. They are the ones treating AI as a structural project, not a software purchase. That means redesigning workflows, bringing the ops team along, and committing to an operating model built for what comes next. The Genius Suite was designed to support exactly that kind of rebuild, one workflow at a time.